經營企業

Global market dynamics: A macro perspective on China (只提供英文版本)

- 經營企業

- 文章

During the JUMPSTARTER Ignition Gala, Jing Liu, Chief Economist for Greater China at HSBC Global Research, delved into China’s recent supportive policy initiatives and their implications on the country’s economic growth prospects.

As China steps up efforts to bolster stable economic growth, the Chinese financial regulators unveiled a raft of monetary stimulus measures in late September 2024. These actions included a reduction in the required reserve ratio and a policy rate cut, as well as an unprecedented liquidity boost to the stock market.

This unexpected move signalled a new era of transparent and coordinated financial policy making. The clear communication of policy intentions and targets prompted an immediate positive reaction in the stock market.

Various departments have since rolled out policies, including local government debt swaps, lowering of down payment ratios and mortgage rates, and the launch of 1 million units of urban village renovation.

China’s real estate market, along with its value chain, accounts for over 20% of China's GDP and holds systemic importance for the macroeconomy. The property correction has weighed on consumer spending and confidence – but easing measures are being introduced and more support is on the way. Local governments now have more discretion on housing policies, including using special bond proceeds to purchase and convert unsold homes into affordable housing. Given the recognition of the housing sector’s systemic importance, the Chinese government will not hesitate to enhance its support if needed.

China’s policymakers are also steering the economy on a new course, from an investment-driven growth model towards a more balanced and sustainable one. Policymakers are becoming pragmatic in facilitating a smooth transition to high-quality growth through structural reforms aimed at fostering sustainable consumption growth in the long term, nurturing high-tech industries and advanced manufacturing, as well as driving green transition.

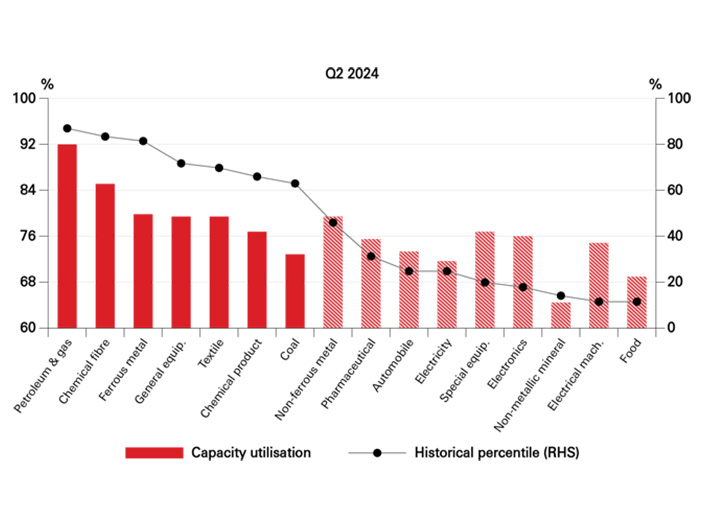

Other than directly stimulating domestic consumption, further policies are anticipated to ‘reflate’ the economy as China continues to grapple with deflation, attributable to varying degrees of excess capacity across industries. Despite the country’s vast population, consumption growth has yet to rebound to pre-pandemic trend.

Source: Wind, HSBC

China’s domestic consumption accounted for less than 40% of the country’s GDP in 2023, lagging behind advanced economies and indicating substantial growth potential. Efforts are being concentrated on boosting domestic consumption and bridging the considerable income gap between urban and rural households. Other than stimulating the demand side, China has other policy options to rebalance supply and demand. For example, the green transition may be a tool to facilitate the consolidation of high-carbon-emission sectors, which have excess capacity due to the housing market correction.

China announced a fiscal stimulus centred around local government debt swaps in early November. While this may appear as an accounting adjustment, it involves injecting fresh capital into the system, which can spur economic activity by enabling local governments to pay their suppliers and employees.

Overall, these coordinated policy efforts reflect a strategic approach to addressing both cyclical and structural challenges in the Chinese economy. By stabilising key sectors, boosting domestic consumption, and promoting sustainable growth, China aims to navigate the complexities of its economic transition amidst a backdrop of shifting global market dynamics.

The Hongkong and Shanghai Banking Corporation Limited (the "Bank") neither endorses nor is responsible for the accuracy or reliability of, and under no circumstances will the Bank be liable for any loss or damage caused by reliance on, any opinion, advice or statement made in this article.